Exercitation ullamco laboris nis aliquip sed conseqrure dolorn repreh deris ptate velit ecepteur duis.

Close

Get in touch

[contact-form-7 id="5" title="Sidebar Newsletter"]WHY SO MANY RICH PEOPLE DON’T FEEL RICH

Articles

Articles

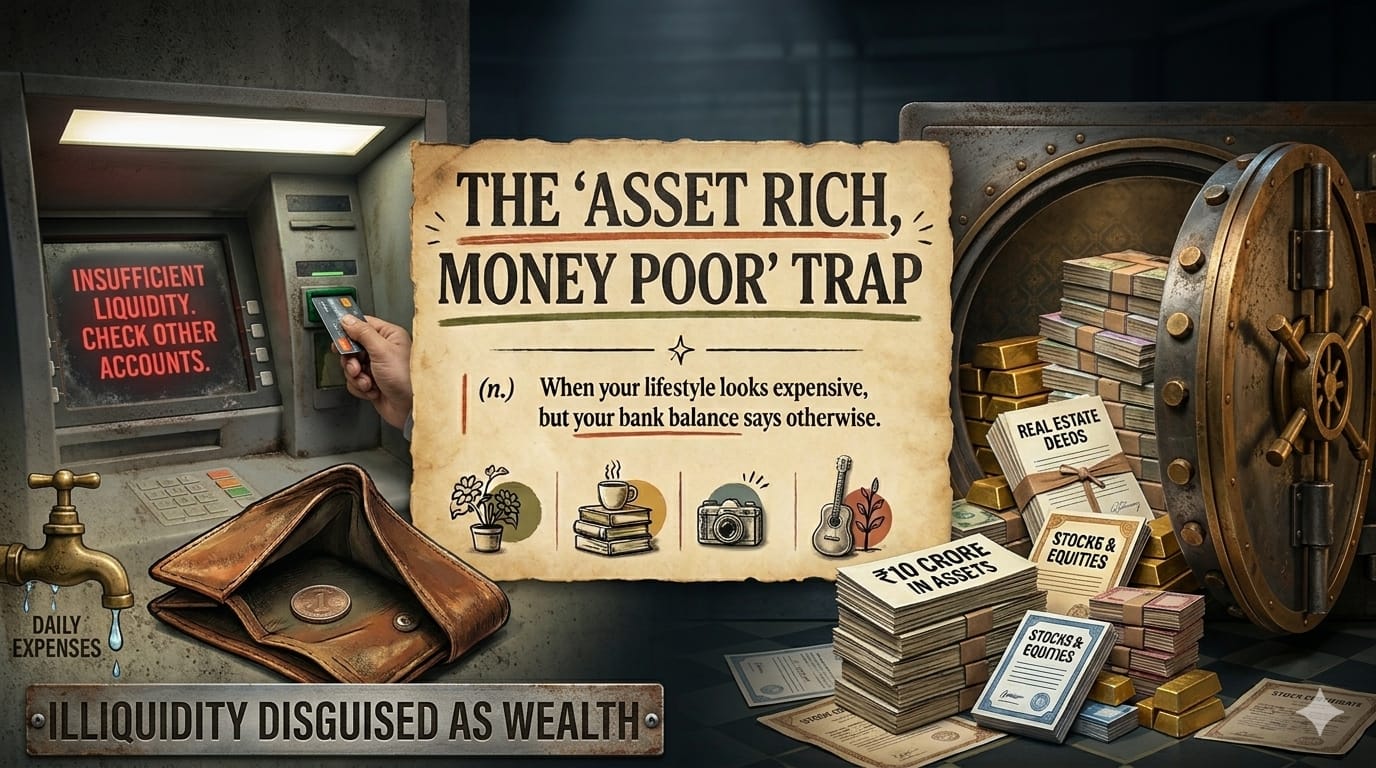

One of the most overlooked financial problems today is not poverty, but illiquidity disguised as wealth.

There are countless people whose net worth comfortably crosses ₹10 crore, yet their daily financial behaviour resembles someone living with constant scarcity. They own multiple assets, maintain diversified portfolios, and have spent years making disciplined financial decisions. On paper, they are wealthy. In practice, many of them do not feel financially free at all.

This is the growing class of people who are wealthy on paper but broke in real life. They have invested everywhere. Real estate, mutual funds, stocks, PMS portfolios, fixed deposits, retirement accounts, gold, inheritance assets, every surplus rupee has been intelligently allocated somewhere. Financial advisors would likely describe them as responsible, disciplined, and financially successful.

Yet, despite all this wealth, a surprising pattern emerges. Many hesitate before taking vacations, many delay lifestyle upgrades for years, many avoid large purchases even when they can technically afford them and if suddenly asked to arrange ₹1 lakh in cash, the response is often the same.. “I’ll have to sell something.” That sentence perfectly captures the contradiction.

The issue is not lack of assets. The issue is lack of accessible money and, more importantly, lack of confidence around spending.

Modern financial culture has trained people exceptionally well in the art of accumulation. Earn more, save aggressively, invest consistently, avoid unnecessary expenses, and let compounding do its work. Over time, this approach creates impressive portfolios and large net worths.

But there is one problem almost nobody talks about, very few people are taught how to live off the wealth they create. As a result, many individuals spend decades building assets without ever building a system that allows them to comfortably use those assets. Their money exists everywhere except in their actual lives.

The apartment worth ₹5 crore cannot fund everyday expenses unless sold or leveraged. The equity portfolio is mentally categorized as “long-term wealth.” Fixed deposits are preserved for emergencies. Retirement funds are considered untouchable. Every investment is tied to a future objective, which means nothing feels safely available for the present.

This creates a strange psychological state where people know they are wealthy but still do not know what they are allowed to spend. Uncertainty around money often creates more stress than lack of money itself.

Many wealthy individuals constantly worry about whether they are making financially irresponsible decisions. A vacation feels like destroying future compounding. Buying a better car feels wasteful. Upgrading lifestyle creates guilt rather than satisfaction.

The portfolio grows, but financial peace does not. This is because wealth and liquidity are not the same thing. Net worth is theoretical and lifestyle is practical.

Someone may technically own ₹10 crore in assets, but if every rupee is locked inside property, long-term investments, or emotionally untouchable accounts, daily financial flexibility remains surprisingly limited. This is the hidden downside of over-optimization.

In the pursuit of maximizing returns, many people unintentionally minimize usability. Every rupee becomes an investment decision. Every expense becomes a debate. Every withdrawal feels dangerous.

Over time, wealth stops feeling like freedom and starts feeling like responsibility. Ironically, society often praises this behaviour. Financial restraint is seen as maturity. Conservative spending habits are celebrated as wisdom. And discipline certainly matters. But there is a fine line between discipline and financial paralysis.

A large number of wealthy individuals are not avoiding spending because they cannot afford it. They are avoiding spending because they do not know if it is safe to. That distinction matters enormously.

Most people understand accumulation but not extraction. They know how to build portfolios, but not how to design sustainable cash flow from those portfolios. They know how to grow wealth, but not how to confidently use wealth without fear of damaging the future. As a result, many remain trapped in a permanent accumulation mindset.

The emotional operating system never changes, even when the balance sheet does. This is why some people with substantial wealth continue living with low-grade financial anxiety for decades. Their assets may grow every year, but mentally they still behave as though one wrong decision could destabilize everything.

And this problem is becoming increasingly common among high earners, business owners, professionals, and inherited wealth families alike.

The financial industry spends enormous time teaching people how to make money. Schools teach earning potential, the internet teaches investing, social media glorifies compounding and aggressive wealth creation. But almost nobody teaches the equally important skill of spending wisely.

Very few discussions focus on questions such as:

- How much can safely be withdrawn every year?

- Do I have an income replacement strategy?

- Which investments are meant for living expenses?

- How much should remain in FD and Real estate?

- At what point does saving stop and spending begin?

Without answers to these questions, people continue accumulating wealth indefinitely while remaining emotionally disconnected from it and perhaps that is the real tragedy.

Money is supposed to create ease, flexibility, experiences, and peace of mind. It is supposed to reduce fear, not intensify it. But when people spend their entire lives only learning how to preserve wealth, they often forget the original purpose of wealth itself.

Financial success is not merely about growing assets endlessly. It is about building a life where money becomes a support system instead of a source of constant hesitation, because ultimately, the goal is not just to become rich on paper, the goal is to feel financially free in real life too.